As of today, March 31, the current price of WTI is just over $100—at $101.50 a barrel. The current target rate of the Federal Reserve is 3.5–3.75%.

When the U.S. first hit Iran, the price of a barrel of oil surged to $71 a barrel. In the second week of the war, Iran retaliated by closing the ever important Strait of Hormuz. Oil surged to $94 a barrel, and around the world central banks started to rethink their interest rate stratagem. What was an interest rate cutting cycle according to some instantly turned into an interest rate debacle.

The real reason markets are down is not because of the war, not because of oil, but because of interest rates.

Interest rates are directly correlated with company earnings. If you are borrowing money—which most companies are—you immediately will be paying more money per dollar you borrow the higher the interest rate is. So when oil spikes, inflation spikes and central banks around the world freeze their cutting cycles.

Let's take a quick look at what the markets are telling us:

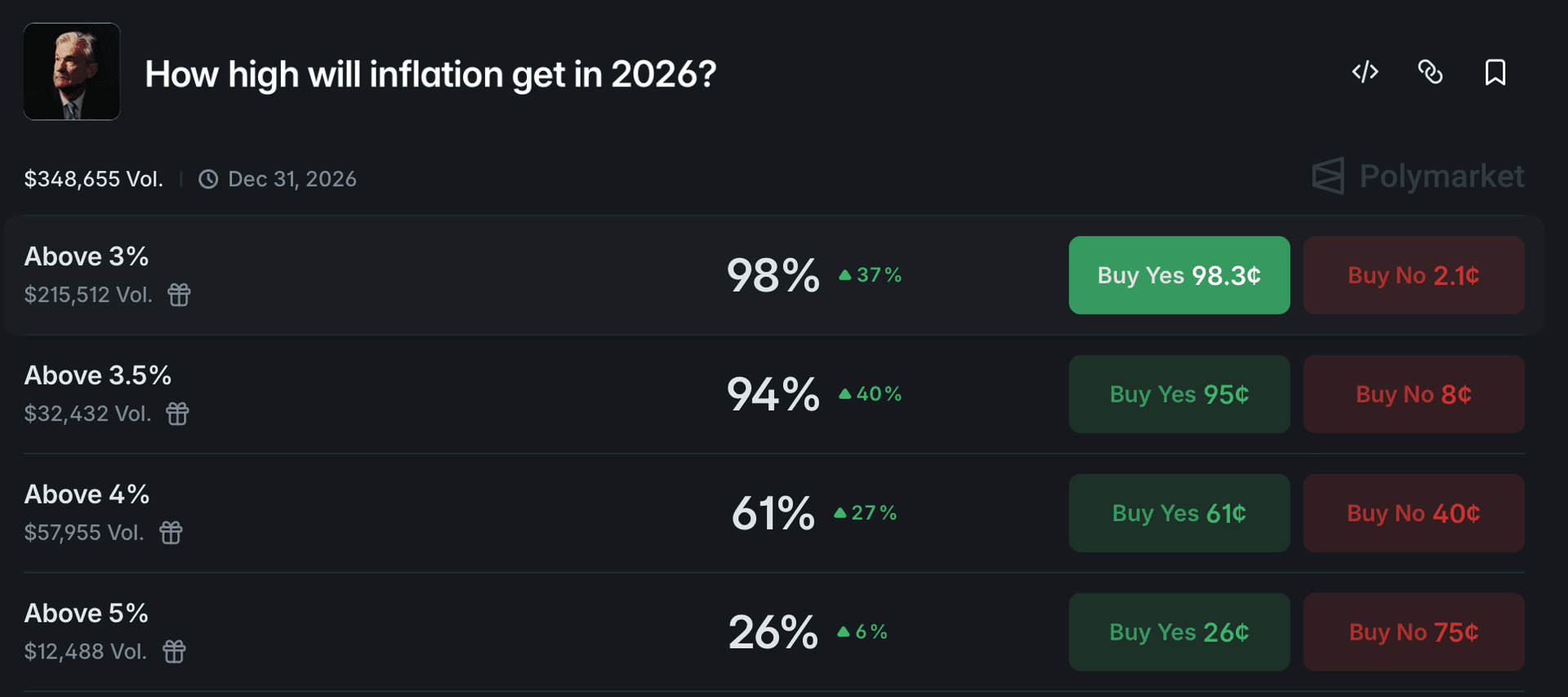

Let's go back to the target rate: 3.5–3.75%.

Jerome Powell and the Fed almost certainly will not cut rates when looking at the numbers we are looking at. Inflation for March is almost surely going to be in the 3–4% range. Inflation above 4% is now projected to be the case sometime this year along with a small probability of 5%.

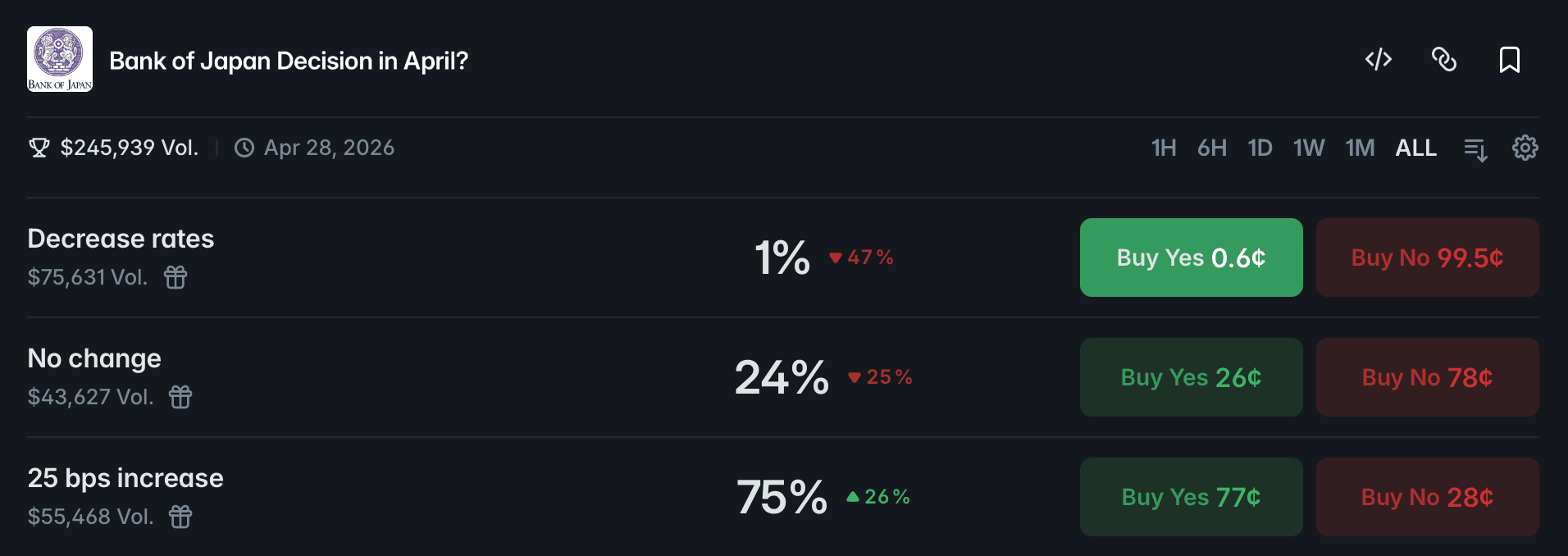

Not only will our Fed hesitate to cut rates, but the No. 2 and No. 3 banks most correlated with the performance of our stock market won't cut rates either. Those banks are the Bank of Japan and the European Central Bank. U.S. investors borrow money from banks with a lower rate than ours, and the Bank of Japan's target rate is 0.75%. When the Bank of Japan is expected to raise rates, U.S. investors panic, sell their assets, and pay back the Bank of Japan before having to pay more at a higher interest rate:

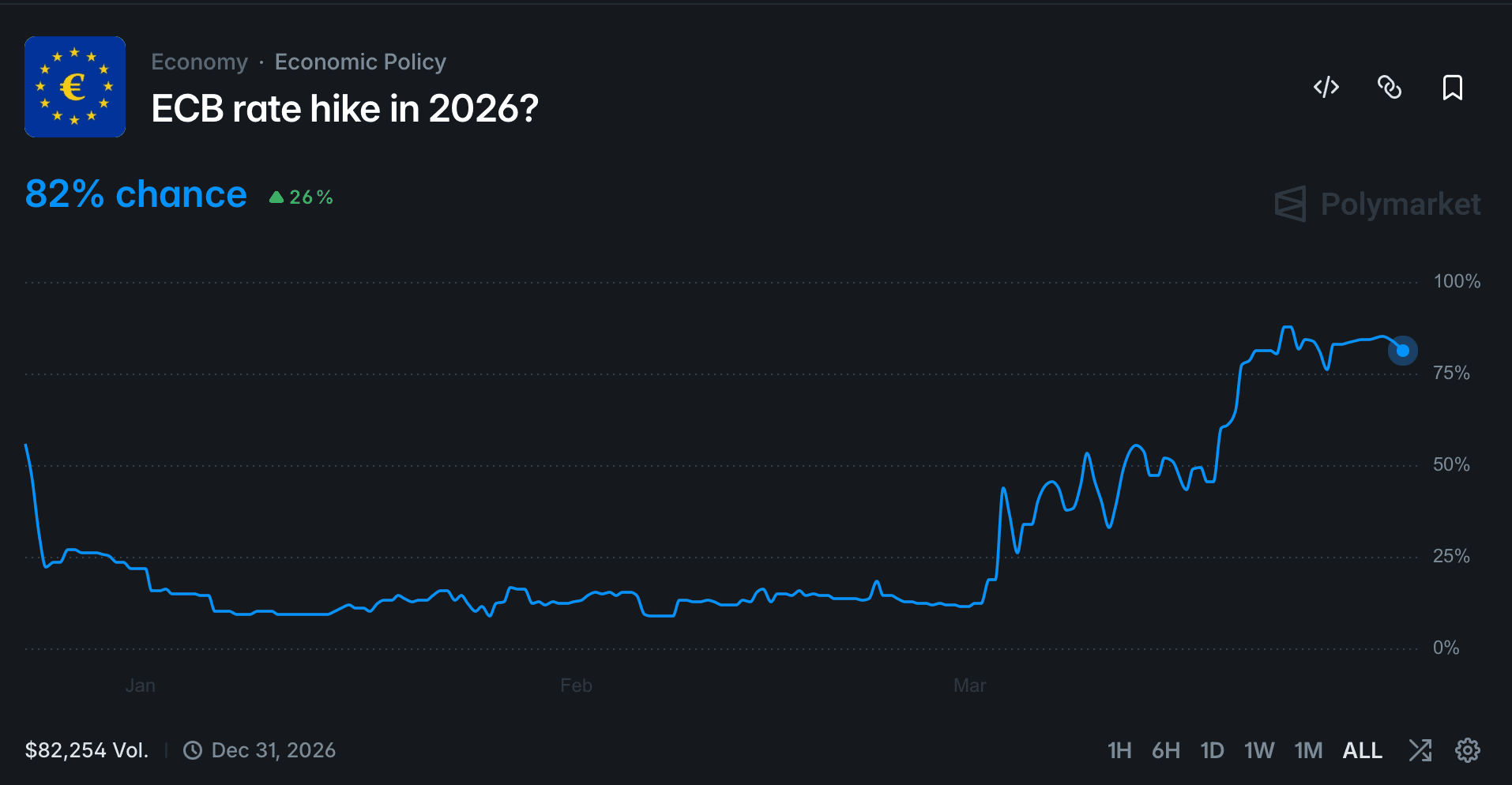

And the ECB:

The three most important central banks in the world as it relates to the health of the U.S. stock market, are all in panic mode. For equity investors counting on cheaper money to fuel earnings growth, it's a nightmare scenario.

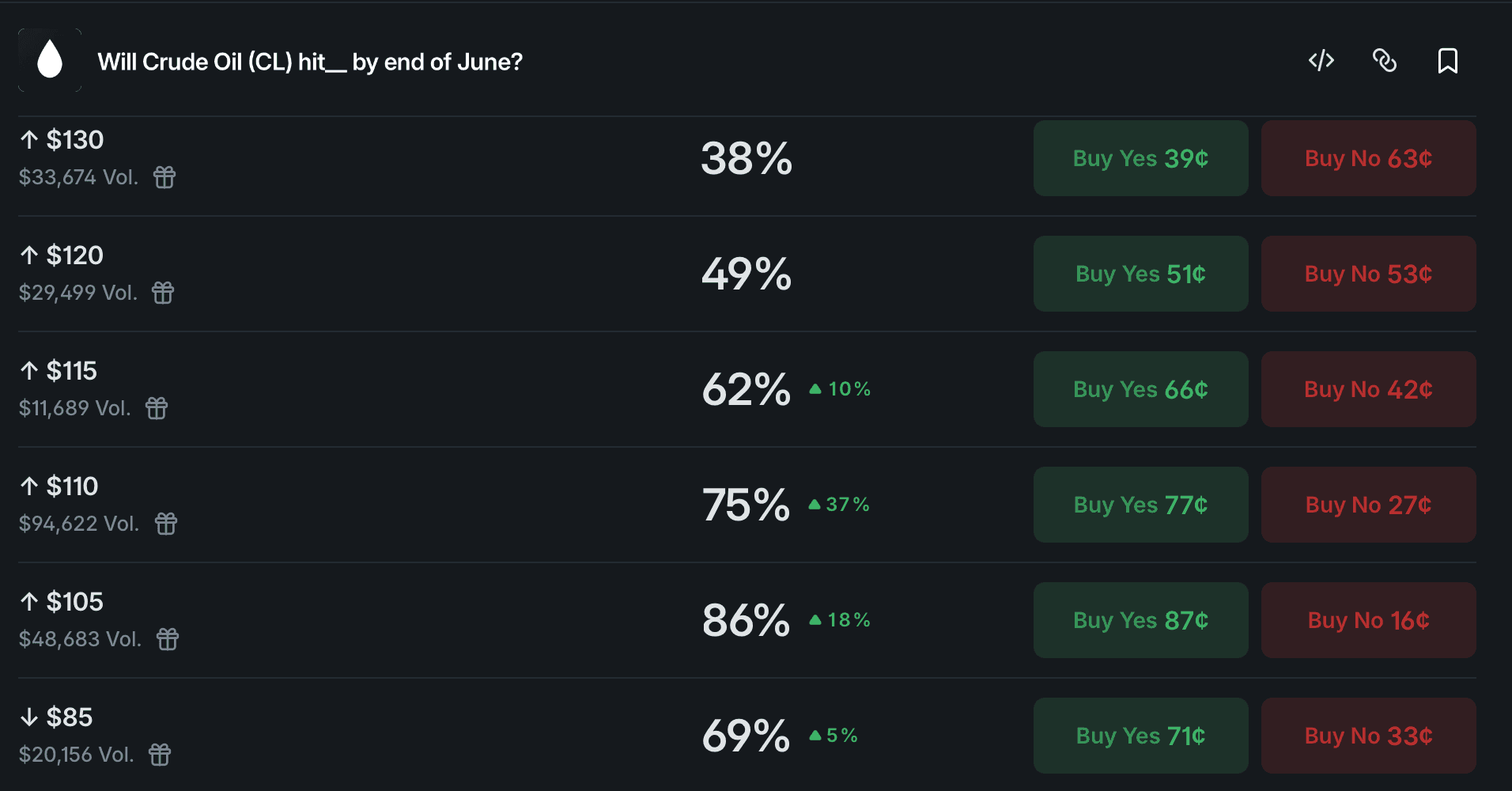

Let's go back to oil, the driver of inflation and consequentially the driver of potentially higher rates:

This tells me two things:

Volatility, but also higher crude in the near term future.

However, with a 67% chance of going back down to $85, one could assume the surge could be a short lived phenomenon.

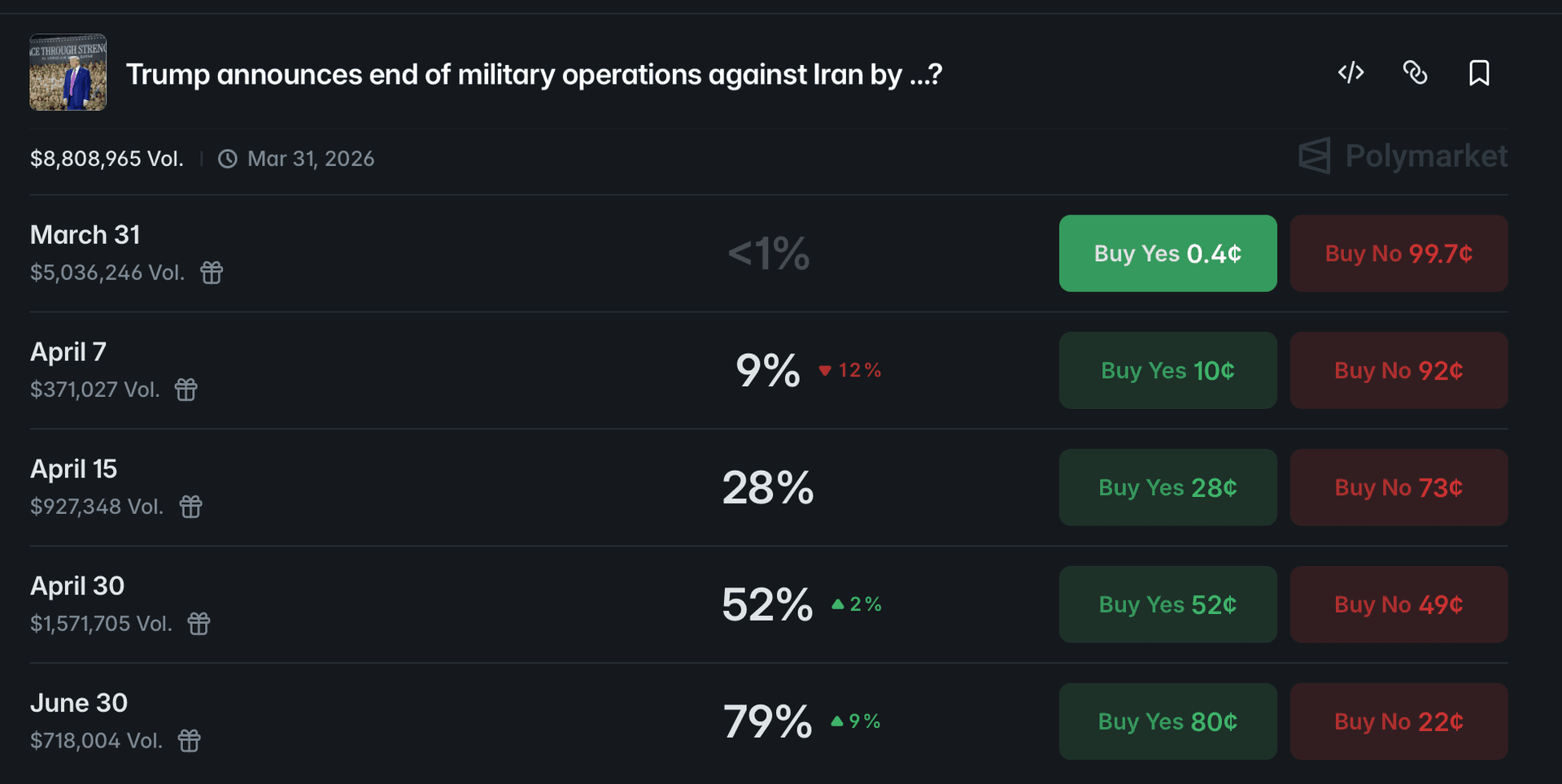

When you pair that with the ending of military operations in Iran, there's more confidence that the price of a barrel of oil will start to come down by the end of June:

Prediction markets are now almost solely the basis of our investment decisions (apart from financials). These markets not only tell us where interest rates are going, but they tell us the projected price of oil, operations in Iran, and to expand on those: the price of SPX, the prices of individual equities, geopolitics, elections and everything in between.